In the world of personal finance, some lessons are learned too late, like when I naively signed up for my first credit card as a college freshman. What if we could equip our children with these vital life skills from the start, preparing them not just for the financial world but for the broader adventures of life? This story begins with two young characters: my 3-year-old and 5-year-old, embarking on their own financial odyssey.

It started innocuously enough. Every trip to Target became a chorus of “Can you buy me this?” followed by a crescendo of “And this? And this?” It dawned on us that something was amiss. While we were fortunate enough to provide for our children, we didn’t want them to grow into stereotypical spoiled brats, blind to the value of money. Besides, our living room and basement, doubling as a playroom, were already drowning in a sea of toys.

Our solution? A job and a weekly paycheck for our toddlers; a departure from the usual allowance system where kids receive money regardless of effort. Our expectations were age-appropriate: picking up toys/ clothes and putting away dishes. My wife, the more stringent of us, even taught them to sweep up their food messes. This wasn’t just about cleanliness; it was about instilling responsibility and the idea that effort reaps rewards.

Weekly wages shown on our refrigerator

Every Saturday (although sometimes I forget and must make it up the following week), I play the role of the benevolent employer, reviewing their ‘work’ and dispensing their earnings of $6 each. Yes, it might seem high for toddlers, but here’s the twist: we introduced them to the concept of investing and charity. Half of their earnings ($3) go straight into their TD Ameritrade investment accounts, planting the seeds of financial growth early. Another $1 is donated during church services, fostering a sense of generosity and community responsibility.

The remaining $2? That’s their spending money, managed through a Till Financial debit card. This transforms every shopping trip into a practical lesson in budgeting and decision-making. (Sign up for Till with my referral code and earn a free $25!) Our daughter has already purchased a see-through backpack, while our son got a toy pizza, a remote control centipede, and a Transformer. It’s more than just buying toys; it’s about understanding the value of money and the satisfaction of earning and spending wisely. Now our son enjoys checking the price tag before asking to make a purchase.

These small steps, these little lessons about money, are our investment in our children’s future. We’re not just teaching them to count coins; we’re instilling values and skills that will serve them for a lifetime. In a world where financial literacy is often learned through the hard knocks of experience, we hope to set our children on a path of informed, responsible financial decision-making, shaping not only their futures but potentially the financial wisdom of generations to come.

Strategies for using compound interest to efficiently pay off debts

In the world of finance, few concepts are as mesmerizing and simultaneously misunderstood as compound interest. It’s the financial world’s equivalent of a double-edged sword. On one hand, it’s the engine behind the growth of investments, and on the other, it’s the silent killer lurking in the shadows of debt. Let’s dive into a tale of triumph, where compound interest, usually the villain in debt stories, becomes the hero helping you escape the clutches of debt.

Picture this: as a young professional, I found myself drowning in credit card debt, a common scenario in today’s spend-now-pay-later culture. I was not alone in this fight; millions are shackled by the heavy chains of high-interest debt. Thankfully my story eventually took a different turn. Instead of succumbing to despair, I harnessed the power of compound interest to break free.

First, I got a grip on my situation. I listed all my debts, noting the interest rates. It’s a scene we’ve seen before: high-interest rates eating away at someone’s financial health. I started by tackling the debt with the highest interest rate — often credit card debt. It’s the financial equivalent of cutting off the head of the monster first.

But how does compound interest play into this? I decided to make more than the minimum payments. Even a small increase in monthly payments can significantly reduce the total interest paid over time. This strategy, known as the avalanche method, targets high-interest debts first, reducing the compound interest accumulating against me.

In addition, you can also explore balance transfer credit cards. These are the financial world’s version of a strategic retreat, regrouping to fight another day under more favorable conditions. By transferring her high-interest debt to a lower interest rate, you can essentially slow down the enemy — compound interest — giving more time to strike it down.

But the real game-changer in my story is my shift in mindset. I started viewing the extra payments not as a loss, but as an investment. Each extra dollar paid towards debt is like a soldier fighting against the compound interest army, gradually turning the tide of the battle in my favor.

And then comes the twist in the tale — I started to invest. Ideally, I would not have waited to be totally debt free. However, I now understand that investing, even small amounts, can grow over time thanks to compound interest. Thus forming an ally with the very force that was once my adversary. It’s a delicate balance, paying off debt and investing simultaneously, but it’s a strategy that can work wonders.

Now, I am debt-free (except for my mortgage), but with a growing investment portfolio. My story is a testament to the power of understanding and using compound interest, not just as a concept in finance, but as a tool in the narrative of one’s financial life. I didn’t just pay off debt; I compounded my way out of it.

Remember, every financial story has its unique twists and turns. But understanding the principles of compound interest and how it impacts debt can be your guiding star. So, whether you’re a young professional or at a different stage in your financial journey, consider how you can turn compound interest from your foe to your ally. In the world of finance, the most gripping stories are those where the underdog emerges victorious, and with the right strategy, that underdog can be you.

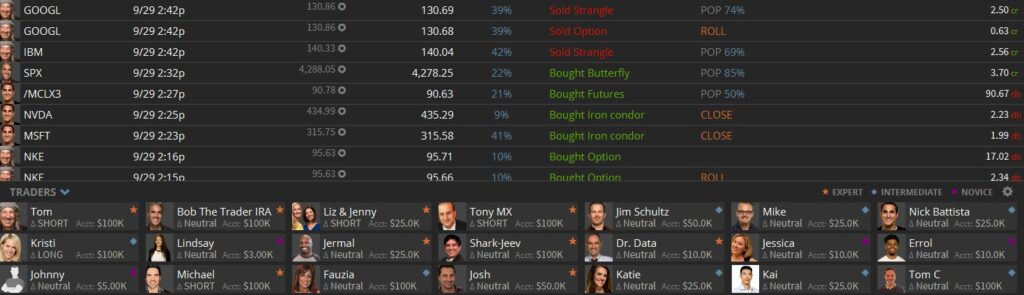

In 2022, I was on top of the world in the trading realm. My main options selling account had netted a 38% annualized return, while the S&P 500 had tumbled by 19%. I strutted into 2023 with a swagger, cockiness in tow. Trading, I thought, was a game I had mastered, and I could almost taste the sweet freedom of retirement. I envisioned myself selling options from a beachside hammock or at least from the comfort of my home office.

Breaking the Cardinal Rule

My strategy was simple yet effective: selling Strangles on individual stocks. The plan was always to exit before earnings announcements, avoiding the heightened volatility they often bring. This strategy hinges on the stock price staying within a specific range, ideally moving sideways, enabling me to collect a profit neatly.

Below is an example of a Strangle: a stock is currently trading at $80, and the expectation is that it will maintain its course within the Strangle’s designated range, between $100 on the upside and $60 on the downside.

Unfortunately, in the spring of 2023, I broke my cardinal rule. Distracted by a work trip to Las Vegas, I left Strangles open on NVIDIA Corp (“NVDA”), a stock mired in artificial intelligence hype with a looming earnings announcement. My initial bet was for NVDA to stay within a $40 range. Little did I know, while I was immersed in the Vegas buzz, NVDA’s stock price was preparing to leap.

The Vegas Surprise

Wrapping up my trip, I was greeted by a financial shock. NVDA’s stock had not just breached my set range but had soared way over the expected move overnight, from around $305 to $379. And it didn’t stop there. Over the next three months, NVDA continued its meteoric rise, peaking around $500. My position, which was once hovering around breakeven, plummeted to a staggering $25,000 loss. Profitability on my overall portfolio seemed like a distant dream.

The Rescue Operation

In a state of panic, I reached out to the CEO of TastyLive (Tom Sosnoff) who replied later that night. (In a world where billionaire CEOs are as accessible as a fortress, the CEO of Tasty stood out with a same-day reply, shining a spotlight on Tastytrade’s unparalleled dedication to their customers.) His advice was consistent: stay mechanical. This meant rolling up puts, extending expiration dates, and waiting for the stock to stabilize. There was some comfort in knowing that I wasn’t alone in this predicament; even Mr. Sosnoff himself was nursing a bad NVDA trade at the time.

Without going into every painstaking detail, employing TastyLive’s mechanics religiously over the following months, I managed to pare down my loss from $25,000 to $3,000.

Deciding to Bail

As NVDA approached another earnings announcement, I faced a decision. I could extend the term and continue wrestling with this volatile stock, hoping to break even or eke out a small profit. However, tired and wary of another potential gap-up and potentially bigger loss, I decided to close the trade and accept a $3,000 loss on this position. After all, another artificial intelligence hype story could easily send NVDA soaring again.

Lessons Learned

This experience was a hard but valuable teacher. Here’s what I took away:

· No More Strangles on Individual Stocks: Especially not on stocks in hot industries like AI. The unpredictability is just too high. I’ve shifted to ETFs, which generally tend to be more stable than individual stocks.

· Stay Vigilant While Traveling: Reducing trades or at least monitoring them closely is crucial. Never neglect the account.

· Stay Small: This principle saved me. My initial NVDA position was just ~1–2% of my buying power in this account, allowing me the flexibility to manage the trade through its tumultuous journey.

· The Power of Options Selling: Unlike buying options, selling gives you tools to maneuver and potentially turn a losing situation around. (Had I purchased an option that turned sour, my only recourse would be to sit tight and cross my fingers, hoping it wouldn’t expire completely worthless.)

Looking Forward

As of now, this options-selling account is only up about 5% this year, trailing the S&P 500’s stellar 20% YTD gain. It is unlikely I’ll hit my target return of 18%; however, I have survived to trade another day. (Conversely, my wife’s retirement account, where we mainly sell Cash Secured Puts and Covered Calls is up an impressive 18%.) This journey has been a testament to resilience in the face of market unpredictability. Happy trading, and remember, the market always has a lesson to teach.

I made the less exciting decision to replace my windshield for $300 and invest the rest

Recently, my accountant completed our extended 2022 tax returns and revealed an unexpected windfall — a $54k tax refund.

It was the most significant refund I had ever received, and it was all thanks to my status as an active investor with a diverse portfolio, which includes an options trading business, real estate, and Bitcoin mining.

The magic of depreciation and expenses

A substantial part of my tax refund came from owning and operating Bitcoin miners. I was able to write off a fair amount of depreciation and expenses on these miners, spreading it over five years.

This is different from investing in residential real estate, which is depreciated over 27.5 years. Additionally, I am able to write off other expenses, like subscriptions to investing publications and office equipment, similar to what a large business can do.

The dilemma of a windfall

With the news of the refund, I was faced with a pleasant dilemma: how should I spend this $54k? Options like paying down our mortgage or taking a vacation seemed tempting.

However, I initially decided to upgrade my 2005 Honda Accord to a used 2022 Kia Telluride SX. My main concern with the Honda was the night driving challenges due to the worn-out windshield.

At night I had to squint my eyes and look at the lines in the road to safely avoid the glare of oncoming traffic.

After putting down a $5k deposit on a vehicle, I realized I was about to make a costly mistake. Instead of splurging $50k on a used SUV, I chose a more financially prudent choice — replacing the Honda’s windshield for $300.

This was a tough decision because I had taken to daydreaming about pulling up to work and social events in this luxury vehicle with its sleek black exterior and smooth black leather interior. However, this choice saved me a significant sum and meant I could invest the $54k into growing our net worth.

Lessons learned from an emotional experience

This journey taught me two valuable lessons about managing sudden financial gains and the allure of consumerism: 1) surround myself with financially savvy people, and 2) keep my eyes on the prize.

Surround myself with financially savvy people

I spoke with a friend contemplating a similar decision with a 3-row SUV. His choice to stick with his existing vehicle and utilize Uber or public transportation when needed resonated with me. In my case, a pricey SUV was an unnecessary luxury. My 18-year-old Honda, with only 130k miles and running smoothly, is adequate for my three times-a-week commute to work.

Keep my ultimate objective in mind

My goal is to retire comfortably and escape the corporate rat race. Spending $50k on a new car would not increase our net worth or cash flow. Investing the $54k in more Bitcoin miners or options trading moves me from being an employee solely reliant on heavily taxed wages to an investor and business owner who benefits from favorable tax treatments.

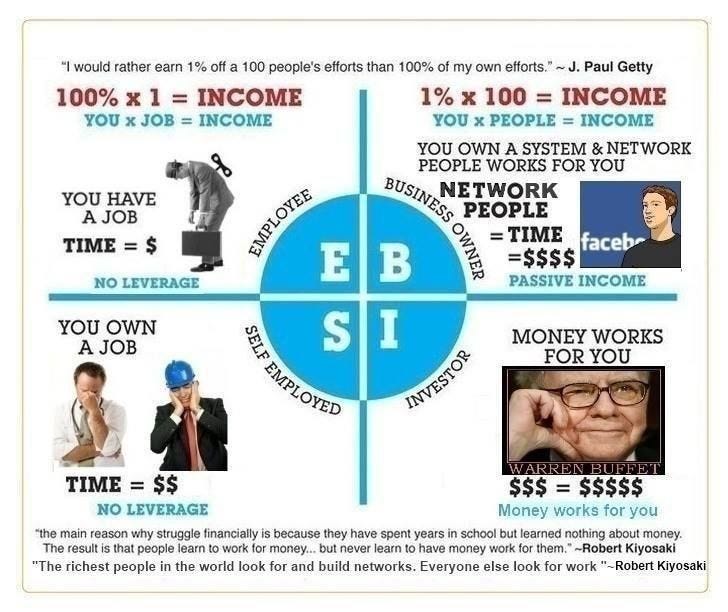

Source: Robert Kiyosaki and fillyourcup

As Robert Kiyosaki, author of Rich Dad Poor Dad, teaches, to obtain wealth and freedom, we should focus on becoming Business Owners and Investors. We can leverage time and systems by having money work for us. (versus trading our time for money)

In conclusion, this experience with the tax refund taught me the importance of financial discipline and the power of making informed decisions. It’s a reminder that the path to financial independence is often paved with prudent, sometimes less exciting, choices.

The Rational Investor was a game-changer for me, unlocking the secrets of managing money like a Wall Street pro.

Early Trading Mistakes

In early 2019, I joined The Rational Investor (“TRI”) community, a decision that marked the turning point in my tumultuous trading journey. Before that pivotal moment, I was just another speculator caught in the frenzied crypto bull market of 2017. My adventure began in the summer of 2017 when Bitcoin was a mere $3,000. Enthralled by the digital gold rush, I rode the Bitcoin rollercoaster to its then-peak of $20,000, only to plummet back down to where I had started without taking any profits. And it wasn’t just Bitcoin; numerous altcoins – which I now refer to as ‘shitcoins’—filled my portfolio showing zero returns. My buying strategy was unsophisticated, often making purchases at the top and watching their value dissolve to nothing.

The madness didn’t end there. Once, a friend’s hot tip on a new crypto token, XRP, had me buying in $0.20. As its value skyrocketed to $3, greed took the driver’s seat; I failed to cash out, and the subsequent fall back down was a harsh lesson in profit-taking—or the lack thereof. Like many novices, I was struck with the affliction of greed, unable to recognize the right time to exit.

My initial foray into trading more than a couple hundred bucks actually began a decade earlier, in 2008. At a trading conference, I won a book on futures trading, and fueled by enthusiasm, I immersed myself in its content. I eagerly funded my trading account with $10,000. Yet, my lack of experience led to a gradual drain to nothingness—I had blown up my account. But back then, being single and holding a well-paying job, I quickly replenished the funds. Inspired by reading Reminiscences of a Stock Operator, which details the life of legendary trader Jesse Livermore, I attempted to emulate his strategy of adding size to winning trades. This approach swelled my $10k to about $160k, only for me to witness a $60k loss in just two days. Devastated, I stepped back from active trading, recognizing a critical gap in my skill set. I was only successful if the market was going up and not truly how to trade sideways or down markets.

Turning Point with The Rational Investor

Fast forwarding back to my rollercoaster in crypto, I subsequently and thankfully came across Davinci Jeremie, an early Bitcoin advocate who, back in 2012, encouraged everyone to buy at least one Bitcoin when it was only a few dollars. While I missed his advice in 2012, I thankfully took his advice in 2019 and sought education at The Rational Investor, where Davinci had honed his trading acumen.

Despite my initial hesitation, I purchased the level 1 course; this proved to be the best investment in my trading education. At the time I purchased the level 1 course, the cost was $1,000 (prices have since marginally increased and remain a great value) and I can readily attest I have made more than $100,000 in trading profits (100x return on the cost of tuition) from my lessons at TRI. This education has been invaluable. I wish I had come across The Rational Investor’s trading courses years earlier versus wasting $100k to attend a top 10 business school where I only learned financial theory. The Rational Investor reshaped my approach to trading from a casual hobby to running my portfolio like a trading business. They taught me about proper position sizing and entry/ exit strategies tailored to my personal trading style.

The beauty of TRI is that while all students take the same curriculum, we are individually attracted to different trading approaches, and we come out with our individual styles and business plans. Over these years I have grown as a trader, shifting from mostly trading crypto to buying options, to now primarily selling options.

I have remained adaptive, ensuring my strategies stay resilient through the ever-evolving financial landscapes. This adaptability and disciplined approach have been constant, no matter how my trading preferences have changed over time.

The impact of this education extends beyond my trading screen. The skills and confidence I gained allowed me to secure a home for my family and provided me with the financial security to know that even in the event of a job loss, I have the means to support my loved ones through trading. Further, the Rational Investor community, ever so supportive, is always there, ready to provide insight and advice, through its trading rooms.

Conclusion

The money spent on The Rational Investor’s courses is, unequivocally, the best money I have ever spent on trading education. It remains one of the best-kept secrets in the world of investing. My journey from financial ruin to a place of stability and growth has not only changed my portfolio; it has changed my life. Happy trading.

In July 2021, I embarked on an ambitious Bitcoin mining journey by pre-ordering my first Bitcoin miner. Fast forward to today, and I’ve invested a whopping $161,000 into purchasing 28 Bitcoin miners, averaging around $5,700 per machine. At the time, it felt like a shrewd move. Bitcoin was hovering around $33,000, not too dissimilar to its current trading range. I was optimistic, believing it had ample runway before it soared to its peak of $69,000 four months later, only to retrace its steps back down.

Best Decision at the Time

Reflecting on this decision, it’s still a toss-up whether it was a stroke of genius or a financial misstep. Since then, I’ve managed to mine about 3 Bitcoin. In contrast, I could have taken a more straightforward route by simply purchasing 5 Bitcoin on an exchange like Coinbase and tucking them away in cold storage.

Had I waited a couple years to buy miners, today’s landscape would allow me to acquire even more potent, next-generation miners, such as the S19k Pro 120 TH for $2,350 each. For the same amount I spent initially, I could amass 68 of these powerful beasts. In comparison, my current fleet ranges from machines with 90 to 110 TH of power. Averaging it out, each of my machines delivers approximately 97 TH or about 19% less power than some newer machines. With newer 120 – 141 TH machines in the market and the impending arrival of 200 TH behemoths (double my mining power), I’m in a race against time to mine as much Bitcoin as possible before my hardware becomes antiquated.

On the surface, this might look like a bad trade. Yet, I remain convinced that over time, I will have mined more Bitcoin than if I had opted to purchase 5 spot Bitcoin. However, this is not without its complexities and uncertainties.

Unforeseen Challenges

I encountered several unforeseen hurdles along the way. Initially, I harbored aspirations of mining from the comfort of my home and later transitioning to an industrial facility. After upgrading my garage’s electrical capacity, I hit a roadblock – my utility provider refused to lower the cost of power, which stood at roughly $0.14 per kWh. This led me to squander about $24,000 between a fruitless garage build-out and equipment to hold the miners, eventually forcing me to relocate those 8 miners to a host charging $0.08 per kWh (42% less).

Another unexpected twist came from Compass Mining. After purchasing 20 miners, I encountered persistent delays in getting the miners operational. Currently, only 13 out of my 20 miners are up and running with them. With each passing day, I miss out on mining fresh new Bitcoin. I learned a valuable lesson to not place too many miners with any single hosting provider.

Benefits of Bitcoin Mining

Despite these unforeseen challenges, I still stand by my recommendation to start mining Bitcoin ASAP. Here’s why:

Inflation Concerns: If you’re worried about rampant inflation, Bitcoin is a must-have asset due to its asymmetric upside potential. Case in point, a Big Mac value meal now costs a staggering $18 in certain locations. As Bitcoin mining difficulty increases each day, it becomes tougher to mine, and the rewards diminish. So, it’s imperative to start as soon as possible, especially with only 9% of Bitcoin left to be mined.

Bitcoin Halving: Each day brings us closer to the next Bitcoin halving. Currently, around 6.25 Bitcoin are mined approximately every 10 minutes. Around April 2024, this reward will halve, and we’ll see only 3.125 Bitcoin mined approximately every 10 minutes. The scarcity factor drove my urgency to start mining ASAP.

Tax Benefits: Much like buying investment real estate, there’s depreciation value in purchasing Bitcoin miners. For residential rental properties, you can depreciate the asset over 27.5 years. For Bitcoin miners, it’s over 1-5 years depending on the accounting method. In my case, we are depreciating ~$32k per annum, which helps to offset my taxable income and contributed to my tax refund for the 2022 tax season. If I had simply bought spot Bitcoin, I would’ve missed out on these tax benefits. Additionally, operating a small mining business allows for deductions on certain expenses like Internet and electricity costs (consult your CPA; not tax advice).

Enhanced Returns: As of today, assuming a 2% difficulty adjustment, I’m turning a profit of approximately $1,974 per month, or $94 per month for each of the 21 miners that are online. This is a snapshot, subject to change based on various factors like difficulty adjustment, Bitcoin’s price (~$35,000 at the time of writing), electricity costs, and of course your miner being online.

This equates to an approximate 15% return on my $161,000 investment per annum. If all 28 miners were online, that’d be around $31.6k in profit annually, or a 20% return – far outstripping the typical 10% return in the stock market. Plus, there’s the added perk of not dealing with the headaches of property management, like fixing toilets.

Conclusion

My strategy is to continue mining through the next halving and up to the subsequent peak, which some predict could surpass $100,000 per Bitcoin. Timing the market is notoriously tricky, but my plan is to sell most of my older miners when demand spikes and supply tightens. Currently, supply is abundant, so if you’re considering mining, now’s the time to start. My goal is to offload these miners close to my purchase price, if feasible. By then, I hope to have mined significantly more than the initial 5 Bitcoins I invested in these miners.

So, to fellow enthusiasts and prospective miners, happy mining, and may your journey be as enriching and educational as mine has been.

For most of my life, saying No has been a challenge. Whether it was a casual invitation for another drink, a request for a financial favor, or a plea from a co-worker for assistance on a project, my default response was invariably, Yes. My old modus operandi was being a people pleaser. The journey to overcoming this habitual Yes and embracing the empowering No, although arduous at times, has been a tremendous improvement in my life and my finances.

Each reluctant Yes subtly eroded my sense of self-worth and inner peace. The fear of disappointing others overshadowed the necessity to uphold my well-being, sometimes emotionally, physically, or financially. I was running away from difficult conversations, fearing the backlash of a simple No.

It took years to transcend this fear and to see the value in asserting my boundaries. Today, one of my daily affirmations is, “to fearlessly face problems collaboratively with love rather than escaping”. I no longer feel the necessity to flee from confrontations. Instead, facing fear is now honorable especially as I am coming towards it with compassion. Further, the dread is usually just a figment of my imagination, often exaggerated compared to the actual reaction. Yes, someone may be disappointed on receiving a No; however, they will be fine. The exercise of saying No, although simple and quick, has been transformative, allowing me to live anew and to assert myself in previously challenging situations.

For instance, my 9-5 job entails selling loans to other financial institutions. In the early days at my company, sleepless nights were a common occurrence as I grappled with the pressure to prove myself, generate outsized profits, and incessantly say Yes to deals. Deals I knew would keep me awake at night. The people pleaser in me wanted to be helpful, but this came at the expense of my emotional and physical health. Over time, I’ve learned to assert a No, especially with the support of data. For example, I declined a recent transaction by pointing out that “I called potential 10 investors and they all said no.” I realize it is alright to push back, to say No when the conditions are not favorable.

The journey towards mastering the art of No also seeped into my personal life, especially concerning financial requests from family. I often felt like a public ATM. Everyone had a sob story. My empathy was exploited to the extent I began to feel a sense of obligation to rescue them from their fiscal miseries. By always giving in, I was enabling their behavior, which was not only detrimental to them but was also draining me emotionally and financially.

At times, when the barrage of requests and expectations become overwhelming, I fantasize about possessing a supervillain-like device to repel everything and everyone, leaving me in peaceful solitude.

Then I realized I do have that power. I get that relief and clarity each time I muster the courage to say No. As Dr. Aziz says, “I am the captain of my own ship.”

Dr. Aziz’s book, Not Nice, illuminated my path toward self-validation. Dr. Aziz had us create a personal Bill of Rights to live by; my first blueprint to live a healthy and assertive life.

A few Rights stand out to me:

I am allowed to say No to anything I don’t want to do, for any reason, without needing to justify it or give an excuse.

I am allowed to not be responsible for others, including their feelings and problems.

I am allowed to change my mind; I do not always need to be logical and consistent.

My family and I are blessed with numerous resources. While I don’t want to morph into a Scrooge, establishing healthy boundaries is imperative for sustaining meaningful relationships and a serene mind. The power of No, wielded with love and understanding, has become a cornerstone of my new way of living.

Achieving financial freedom is not complicated. It, however, does take time. It’s all about creating a plan and sticking to it. I wish someone had taught me this in high school or college. Thankfully, I came across Dave Ramsey 11 years ago, and that kickstarted my journey. However, it took me another few years to discover the FIRE (Financial Independence, Retire Early) movement. If I had to do it all over again, I would have focused on achieving financial freedom as soon as possible. In this blog post, I’ll share my take on the five steps to financial freedom, combining wisdom from different financial philosophies.

Step One: Start an Emergency Fund

The first step is crucial. Start by setting up an emergency fund of at least $1,000. I heard a statistic that most people do not have access to $1,000 if an emergency strikes. Having this cushion will provide the peace of mind to tackle the next steps in your journey. In addition, this buffer will reduce the temptation to dip into your investment account for any unexpected purchases. It’s like a safety net that keeps you from financial strain when life throws a curveball your way.

Step Two: Pay Down Debt While You Invest

Dave Ramsey advises paying off non-mortgage debt before investing; however, I now believe in a balanced approach. I particularly like the 10x Rule from Financial Samurai. This rule suggests paying down any debt by 10x the interest rate being charged and investing any remaining free cash flow. For example, if you have a student loan with a 2% interest rate, allocate 20% of your extra cash to paying down the debt and invest the remaining 80%. This strategy allows you to grow your wealth while also becoming debt-free.

Step Three: Invest 10% to 50% of Your Income

Here’s where the rubber meets the road. You need to invest at least 10% to 50% of your income in a non-retirement account. In my opinion, you should contribute just enough to your 401(k) to get the employer match and no more. Forgo the IRA for the time being. Instead, channel your resources into your non-retirement account to optimize your financial freedom. You can’t easily access money in retirement accounts like IRAs and 401(k)s before you reach a certain age, typically 59½, without incurring penalties. You need to build enough passive income in non-retirement accounts so you can retire early if you choose.

If I were just starting out, I would set up an automatic investment plan into a diversified, low correlated, portfolio of up to five ETFs. For example, consider investing in the following ETFs:

SPY (stock market index that measures the performance of 500 of the largest companies listed on stock exchanges in the United States). Average return since inception of 10% per annum.

BITO (Bitcoin futures ETF) with only a 0.30 correlation to the S&P 500

XLE (energy ETF) with only a 0.28 correlation to the S&P 500

IYR (real estate ETF) with a 0.66 correlation to the S&P 500

I would invest in these funds every time I got paid, regardless of what was happening in the overall stock market – bear or bull market.

Step Four: Let Compound Interest Work Its Magic

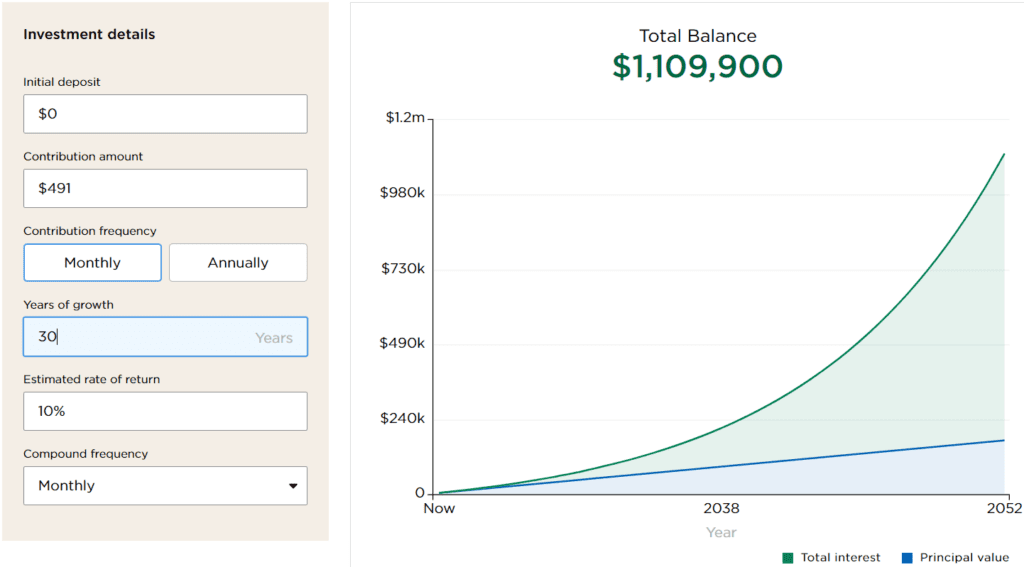

Compound interest is your best friend on the road to financial freedom. To put this into perspective, according to the US Bureau of Labor Statistics, the average income per person is approximately $59k. If you invest just 10% of that income ($491 per month), assuming a 10% annual return, you will have $1 million in liquid assets in 30 years.

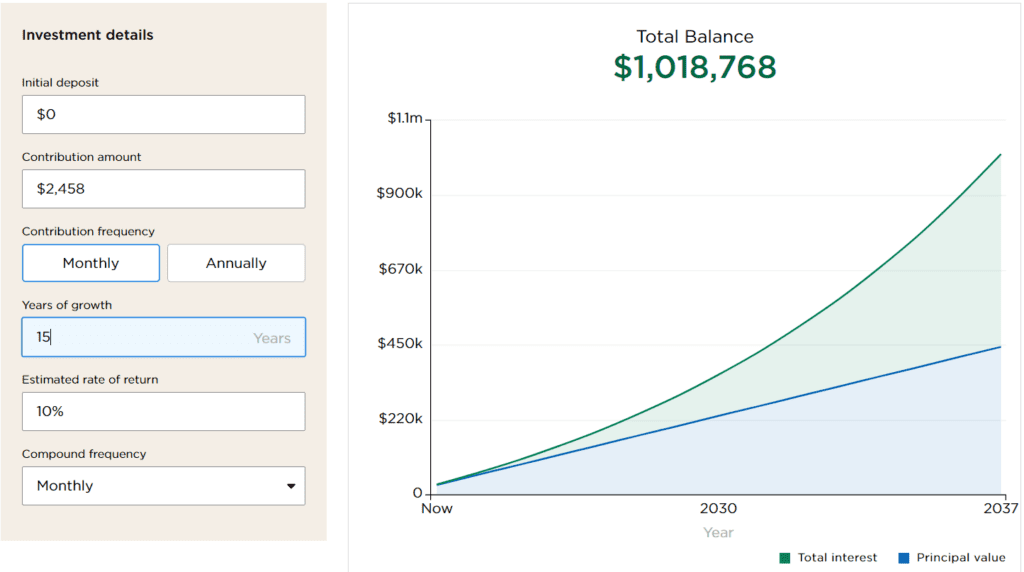

If you go all out and invest 50% of your income ($2,458 per month), you will reach that $1 million milestone in just 15 years. I wish I had begun this way 22 years ago when I started working; however, it’s never too late to begin.

Step Five: Optional Steps for Enhanced Financial Freedom

This step is for those who want to take their wealth-building to the next level. You could learn to sell options like I do, mine Bitcoin, or even start a small business. The goal is to find ways to maximize your returns. For example, by actively selling options, you can reasonably expect to make at least an 18% annual return (~2x passively investing). Alternatively, you could invest in real estate or any other ventures that interest you.

Conclusion

The key to financial freedom is to start investing and to stick to the plan. Whether you’re following Dave Ramsey, the FIRE movement, or my approach, the most important thing is to start and stay consistent. Your future self will thank you. As someone who’s navigated through various financial philosophies, I can say that while the journey may be long, the destination is worth it.

I have walked a long, winding road when it comes to money. In fact, for the longest time, my relationship with money was not just complicated; it was downright dysfunctional. It has been a rocky journey, but I have finally reached a point where I can confidently say I have developed a healthy money mindset. Just as regular exercise is essential for maintaining a healthy body, I must consistently cultivate my relationship with my finances. Here is how it all happened.

The Unhealthy Start

Like too many people, I did not grow up with an ideal model for handling finances. While I grew up in a hardworking, blue-collar, immigrant family, money was often tight, and discussions about finances were scarce. When money was talked about, it was usually to complain about not having enough or being burdened by credit card debt. The absence of a healthy financial dialogue in my household set the stage for my own money missteps as an adult.

College Debt and Early Adulthood

When I was a freshman in college, I got my first credit card. Banks were practically throwing cards at students, and I was no exception. I maxed out that card almost immediately; it had a limit of around $300. I recall the struggle to pay off this debt, given the limited hours I worked at the campus dining hall.

After graduation, I entered the workforce with an initial salary of around $60k – more money than I had ever seen in my account. The irony is, I had majored in economics and worked in finance; however, I still had no discipline with personal finances. I was a full-on consumer: car loan, unchecked spending, and a nonchalant attitude toward my $20k in student loans. I was making money, but I was not properly managing it.

My Wake-Up Call

Life has a way of throwing curveballs, and mine came around the time of the Great Financial Crisis of 2007-2008. My company stopped doing any new business. I was not laid off, but I could see the writing on the wall. That was the first year I did not get an annual bonus, which was usually over six figures. That year, I got what we called a donut (because it is shaped like a zero). I usually spent beyond my means and heavily relied on that annual bonus to payoff any outstanding debt. Now I was stuck with tens of thousands of dollars in credit card debt. In addition, I was still carrying my ~$20k in undergrad student loans, which I could have easily repaid in better times.

Feeling lost and unsure of my future, I decided to go back to school for my MBA. Despite landing a fellowship that covered tuition, I continued to live beyond my means, taking on more debt to cover living expenses. I was a ticking time bomb.

Before going to business school, I had hired a financial planner but made no progress. I eventually drained my IRA which had peaked around $250k, treating it like an extra bank account. I was desperate, hitting rock bottom. As a last resort, I signed up for food stamps (a month before I found a new job in finance). I remember waiting in line to sign up for food stamps; hoping no one would recognize me. In line at the grocery store, I nervously swiped the distinctively white government issued card. Later that day, someone texted and asked if I was just at the grocery store. Embarrassed, I replied yes. Despite lowering the brim of my New York Yankees hat, I was still spotted.

My Turning Point

Desperation led me to seek meaning beyond myself. I finally realized what I was seeking. I was seeking freedom from compulsive negative habits, not material possessions. I finally realized my financial ruin was just a symptom of my underlying emotional dysfunction with money and life.

In a desperate attempt to find meaning beyond myself, I began attending church, where the congregation just so happened to be reading Dave Ramsey’s The Total Money Makeover. I was inspired to take control of my financial destiny. I started listening to Dave Ramsey’s podcast every day, drawing inspiration from others who had struggled with debt and came out on top. I loved hearing callers scream “I’m debt free!” As Dave says “Money is 80% behavior, 20% head knowledge. It’s what you do, not what you know.” I needed to address the negative habits of my financial life.

My Key Takeaways

Emotional Fitness First: I had to get my emotional and spiritual fitness in order before I could tackle the numbers. I needed a strong why; a reason to change my financial habits.

Seek a Plan: I needed guidance. Thankfully, I stumbled across Dave Ramsey and then hired a financial advisor. Although I later took control of my own finances (see link), the experience forced me to think about my retirement age and future financial goals.

The Power of “No”: Being broke taught me to say no. I stopped being the ATM for friends and family, which was a silver lining in my financial struggles.

Emotional Healing: I knew I needed something greater than myself to change my actions. I came across a book called 10-Day Money Makeover, which focuses on improving my relationship with money through the practice of the Emotional Freedom Technique (EFT). EFT is a technique that involves tapping on specific points on my body (like under my eyes) with my fingertips while focusing on negative emotions or physical sensations to release emotional blockages. This was an early and crucial step in developing a healthy money mindset.

A New Chapter

Today, I have developed a healthy relationship with money. I have turned the page on my past financial misadventures and am now focused on a stable and prosperous future. If you are struggling with money, you do not have to hit rock bottom to start turning things around. A healthy financial life is possible, and the first step is deciding whether you are ready for a change.

Ever heard of the Fold App? I’m here to share my journey of how I use this ingenious application (and debit card) to stack Bitcoin with my everyday purchases, turning pennies into thousands. In fact, I’ve earned a whopping $10,000 just by using this app for my regular shopping!

On my journey to financial independence, I’m always on the lookout for ways to earn, save, and grow my investments. Fold is an integral part of my financial freedom strategy.

Getting Started with Fold App

If you’re new to Fold, signing up is a breeze. If you use my referral link to sign up, Fold will gift you a generous 20,000 Satoshis (0.0002 Bitcoin) to kickstart your journey. That’s already a win in my book!

Now, while there’s a free version of Fold available, I personally vouch for Spin+, which costs $100 annually to maximize returns. Why? Well, in the span of roughly 46 months since I jumped on the Fold bandwagon, I’ve managed to earn approximately 36.4 million Satoshis. That equates to ~$10,000 given the current price of Bitcoin. Try out this handy Bitcoin Calculator to check the worth of your Bitcoin.

The Future of Bitcoin and Fold

Now, I’m no fortune teller; however, given past trends, I firmly believe during the next Bitcoin bull run, we will see Bitcoin test its previous all-time high of $69,000. Click here to read more. If that happens, the Bitcoin I’ve earned from Fold could easily surpass $25,000. Imagine that – my Fold rewards paying for a significant portion of my past purchases!

How I Use Fold: The Amazon Example

A significant chunk of my Fold rewards comes from Amazon purchases. Who doesn’t shop on Amazon? From cleaning supplies and toys for my kids to groceries from Whole Foods, I’ve been racking up the rewards.

Here’s a quick rundown of a recent $25 gift card purchase for Amazon:

Step 1: First things first, download the Fold app. And then purchase the Amazon gift card via Fold. Upon this purchase, I earn 2.5% back in Bitcoin. In addition, each $10 purchase results in a spin on the Wheel for chances to earn even more Bitcoin, including a full Bitcoin!

For my $25 gift card purchase, I instantly earned 2.5% back (2,114 Satoshi or roughly $0.60 depending on Bitcoin’s price). Plus, I received some spins on the Wheel.

Step 2: Copy the claim code into the Amazon app. Or select the Redeem Now button for faster processing. It’s that simple.

Step 3: Go back to the Fold app and spin the Wheel to earn some additional Bitcoin and for a chance to win a full Bitcoin.

Other Benefits of Fold App

We have also started paying our hefty mortgage using using our Fold card through PayPal. There are a couple of hoops to jump through, but the rewards make it entirely worthwhile. By using this PayPal hack, I get 0.5% back for various bills like mortgage, rent, auto loans, student loans, phone, and utilities, etc. Just to give you an idea: for my monthly mortgage payment of $5,423, I earn back approximately $25 (or 89,847 Satoshis) plus a staggering 542 spins. That’s 542 chances to win more Bitcoin!

Step 1: First pay your utilities using PayPal (which is linked to the Fold debt card) and earn 0.5% back in Bitcoin.

Step 2: Head over to the Fold app, and spin the Wheel for 542 chances to stack more Bitcoin!

Boosting My Earnings with Fold

Fold recently introduced Category Boosts, which give additional percentages back on certain categories. Currently, I get 2% back on rideshares & taxis and 1.5% on restaurant purchases.

And then there are Merchant Boosts. These are massive percentage kickbacks from popular stores without needing to buy a gift card. For instance, I enjoy 15% back from Disney+ and ESPN+, 3.8% from Starbucks, and even 2.3% back from the likes of Hulu and Netflix.

The best part is I can combine both Merchant and Category Boosts. So if I get 3.8% back at Starbucks and an additional 1.5% for it being a restaurant purchase, I’m looking at a 5.3% total reward on just one Starbucks buy!

Securing My Earnings

Lastly, each month, I transfer the Bitcoin I’ve earned from Fold into my cold wallet. It’s a simple step, but it ensures my earnings are safe and secure.

If you’re not on Fold yet, I’d say it’s about time. Sign up. It’s been a transformative tool in my financial freedom journey, turning everyday purchases into sizable rewards. Why leave money on the table when you can fold it into your wallet?

I first learned of tastytrade in late 2019. It would, however, take me a couple of years to finally open an account. I spent those years wasting money on books, options courses, and fees on other trading platforms before finally opening an account at tastytrade. Learn from my mistakes and don’t waste another minute or dollar buying expensive options trading courses. At least, before you decide, take a look at the priceless (yet free) educational content on tastylive, and then open an account on tastytrade. These are the best places for any active options traders.

Streamlined User Interface

In 2020, during the pandemic, I started working from home, and decided to open an options trading account at a couple of different brokerages. I wanted to create an additional income stream to contribute to my financial independence.

I unfortunately delayed opening an account at tastytrade and instead opted for the larger and more widely recognized platforms, one of which already held my retirement funds. However, I found these other platforms (Fidelity and Interactive Brokers) to be clunky, confusing or both. Tastytrade is like the Apple iPhone of trading platforms with its seamless and intuitive user interface. It almost feels second nature.

For example, on Fidelity, I had to inefficiently open multiple windows to enter a simple options trade. Similarly, while Interactive Brokers does offer more products than tastytrade (including orange juice futures), for all of Interactive Brokers’ power, it can be a bit clucky and confusing. For example, it took multiple phone calls to support and tinkering with the platform to finally find the beta weighted delta of my portfolio; something readily streamlined into the user interface of the tastytrade platform.

Useful Educational Content

More importantly both Fidelity and Interactive Brokers lack thought leadership and independent research on how to optimize and efficiently manage risk. While using these less streamlined platforms, I constantly found myself consuming research on tastylive to learn the mechanics and strategies of trading.

Tastylive is a think-tank that goes beyond the typical brokerage experience. They provide live daily commentary and research content that helps me to consistently make profits. Tasty’s research often involves back-testing different trading strategies, running simulations, and evaluating market statistics to form conclusions. This is a much more data-driven approach to understanding financial markets, and it is designed to help investors and traders make more informed decisions.

I have binge-watched all the past episodes of Best Practices, Options Jive, and Market Measures; I recommend you do the same. These programs helped me to learn trading strategies and to properly manage risk. I now comfortably and consistently manage winners, and I don’t panic when some positions are inevitably challenged. I have also watched every episode of Rising Stars, which inspires me to see retail investors, such as myself, be successful using the Tasty mechanics.

Finally, in the summer of 2022 I went fully into actively selling options on tastytrade. I funded my margin trading account with around $200k in June 2022. In six months of selling options, I made a return of roughly $38k or about a 19% return (38% annualized). Meanwhile, the S&P lost 18%. I was hooked and knew this was my way to financial independence.

According to research at tastylive, an actively managed account can reasonably expect to consistently make an 18% return, which is 2-3x the return of passively investing in the stock market or approximately 4x the risk-free return (see link). For the first time (since discovering Bitcoin), I realized I have the tools to escape the corporate rat race and to earn my way to financial freedom with actively selling options.

I had found the holy grail – a way to consistently generate income from selling options. After seeing numerous people laid off during the pandemic (including my former boss and a colleague), it felt good to know I could support my family with selling options if I ever unfortunately lose my 9-5.

Watchlists

I remember wasting money buying lists of daily options trades. Don’t waste your money. The tastytrade platform has built-in watchlists to keep you engaged. Whether you are looking to trade earnings, high implied volatility or futures, tastytrade makes it seamless to find a viable trade. In addition, there is a Follow page, where you can see real-time trades of the expert options traders at Tasty.

Each day, I enter one or two new trades. I first check the various watchlists and if nothing meets my criteria, I check the Follow page to see what trades the Tasty personalities have put on. Unlike day trading, I don’t have to watch the markets all day, and it takes less than 30 minutes to research and to execute a new trade or two each day. This is great because I still work a 9-5. I typically have 10-20 positions in my margin trading account, and given how seamless the platform is, I efficiently scan, monitor, and manage any existing positions.

Customer Service and Connection

The customer service at tastytrade is outstanding. Whether I have a question about a complex options strategy or need help navigating the platform, the support team is prompt and knowledgeable. I have even emailed the CEO of tastylive (Tom Sosnoff) and other tastylive personalities like Dr. Jim Schultz, and they have always provided a response the same or next day at most. Also, since joining Tasty, I have attended two live events in NYC, which are fantastic.

Conclusion

Tasty has given me the tools, know-how, and confidence to grow my investment portfolio. It is empowering to know I have another stream of income to support my family by selling options. If you’re keen on embarking on a similar journey, don’t waste time and money like I did initially. Dive into the wealth of information that tastylive offers for free and get trading on tastytrade!

In 2003, a couple years after I had graduated from college, I bought a 3-unit rental property in my hometown in Connecticut. I was young, eager, and ready to dive into the world of real estate investing. The problem was, at the time, I was living about two hours away in Boston with plans of moving back to my hometown to be closer to my then-girlfriend. I was intending to house-hack (live on the third floor and rent out the other two units to live rent-free). However, I was working in Boston, and my company ultimately denied my request to move. Further, my relationship with my then-girlfriend had gotten rocky, so I made a major pivot and moved to New York City. Now being almost three hours away, being a long-distance landlord quickly lost its appeal to me. NYC was filled with much more stimuli, and I spiraled into constantly going out – wasting precious money, time, and energy.

Early Mistakes as a Landlord

The few hundred dollars in monthly profits struggled to keep my interest. The only real upside was the income covered my car note on a slightly used Acura TL S (much nicer than the 2005 Honda Accord I currently drive). I also dreaded the constant need to fix things at the property and the hassles of dealing with tenants.

In fact, shortly after closing, I hired a general contractor (who just so happened to be my uncle) for some repairs. Being naïve, I did not even have a written contract. He verbally quoted me ~$6,000 for the work, but by the end of the project, he had added another $6,000 to the bill. I went from having a $6,000 buffer to zero savings. A few years later I sold the property to my sister, where I essentially broke even.

Free of my responsibilities as a landlord, my life continued to nosedive. It would take almost a decade to turn my life around and a few more years before I ventured back into being a landlord. At this point I had developed a healthier relationship with money and my credit score was slowly improving.

In 2016, my sister and I purchased a 6-unit fixer upper for $145k in Connecticut. We put in at least another $100k of cash equity and numerous hours of sweat equity. I was naïve to think it would be like a HGTV episode where we fully gut renovate in only 30 days; 6+ months later we were finally done with the major repairs and ready to start leasing.

Ideally, we would have started with a more turnkey property. However, my credit score was still suboptimal, so we were unable to obtain traditional financing. After some twists and turns, we wound up at a community development fund that provided a mortgage with rates double that of a traditional bank. Not optimal; however, we were momentarily happy to be back in the real estate game. (Will write a separate post of this experience; however, we ultimately sold this property.) It should have been a cash cow; however, there was some overuse of the expense account by my partner, and I continued to dread dealing with the ever revolving door of tenants and upkeep.

I ultimately realized that unless I can invest enough capital to acquire a much larger property with a strong management team, or unless I am house hacking, or I have enough energy to hustle as a fulltime landlord, I am better off investing in crowdfunded real estate.

The benefits of investing in crowdfunded real estate include 1) minimal time and monetary commitment 2) more liquidity, and 3) diversification. Let us explore further.

Minimal Time and Monetary Commitment

A couple of months ago, I opened an account at Fundrise. You can start investing with as little as $10 on Fundrise. I contribute about $400 per month. We invest in what Fundrise calls a Balanced Investing Plan, which seeks to build wealth through investing in assets that provide a mix of cash flow and appreciation in value. Fundrise also offers other plans that focus more on generating cash flow or asset appreciation; there is even a fund that focuses on tech companies in the real estate space.

Per Fundrise, the projected return of the Balanced Investing Plan ranges from 6.5% to 15.3% per annum. Assuming I continue to invest $400 per month, in 22 years, my projected return is $369k.

Another benefit of investing in crowdfunded real estate is we still receive the tax benefit of depreciation, which helps to offset passive income. In addition, crowdsourced real estate offers pass through taxation, meaning income and losses are generally passed directly to investors, which means you can offset other income with losses, if any, from your real estate investments. (Unlike publicly traded REITs, which do not offer the benefits of depreciation or pass-through taxation.)

One of the most attractive features of crowdfunded real estate is the minimal time commitment. There is no need to manage properties, collect rents, evict tenants, renovate units, or deal with insurance claims and legal entities. I still reluctantly own a 2-family property in Connecticut. I have so much going on in my life (family, work) that spending even an hour dealing with tenants or contractors feels like a time drain.

More Liquidity

Fundrise allows you to redeem your investments on a quarterly basis. This is in stark contrast to my experience of trying to sell the aforementioned 2-unit property for 12 months without success. After wasting thousands of dollars on moving out a tenant and on repairs, several buyers were ultimately unable to secure financing. So I unwillingly continue to be a landlord, for now.

Diversification

I have only ever owned investment properties in Connecticut as a landlord. Thankfully, with platforms like Fundrise, I can diversify my real estate holdings. Now, I own a diverse pool of assets like single-family rentals, multifamily rentals, and industrial properties in strong markets across the country.

Challenges of Real Estate Crowdfunding

The counterpoint of only investing in crowdsourced real estate is you are not able to fully capture tax benefits, such as writing off expenses for travel, meals etc.

In addition, by only investing in platforms such as FundRise, you may miss out on directly purchasing undervalued assets you could find at foreclosure auctions. I have personally found properties, which have tripled in value in just 3-5 years. In 2017, we purchased the 2-family property for $89k. We have already done two cash out refinances, so technically we have fully recouped any cash equity and the rest is all profit. The challenge as mentioned, is that while the property appraised for $270k (3x the original purchase), it is proving illiquid to sell and somewhat time-consuming. Being a landlord requires a significant time commitment and hustle. As I get older, I instead prefer to sell options from the comfort of my home to generate consistent passive income.

So, there you have it. Unless you are able to invest heavily and hire an experienced property management team, or to roll up your sleeves and hustle, crowdfunded real estate offers a hassle-free and flexible alternative. You still get certain tax benefits, and you do not have to deal with the day-to-day management of properties. It has been a game-changer for me, and it might be for you too.